07 June 2022

TOPIC: Tax Deductions Vs. Tax Credits

This is one of many guides that teaches you how our tax system works.

If you like guides like this, feel free to follow us on social media and subscribe to our email list to get updates on when a new blog drops!

Lucky you! You just landed on a complete guide to deductions and tax credits.

After reading this, you will have a full understanding of tax deductions and tax credits, and which one will be right for you.

When on your journey to tax freedom, it’s crucial to educate yourself to truly understand how the tax system works.

So, let’s get started, shall we?

What Are Tax Deductions?

Tax deductions were first introduced in 1862. During that time, President Abraham Lincoln signed a bill called the Revenue Act of 1862.

This bill temporarily made Americans pay income tax to fund the Civil War. What was included in this bill was deductions for state, local, and national taxes.

Nowadays, tax deductions are obtained from reporting business expenses and personal losses.

They function as a tax incentive to reduce the burden of owning a business.

In a nutshell, tax deductions reduce the amount of taxable income a person has.

For those who are more visual, look at the illustration below.

Note: Normally, no matter what tax bracket you land in, you will never pay the full percentage listed on that bracket.

But for the sake of this illustration, we are going to ignore how our progressive tax system works to make this concept easier to understand.

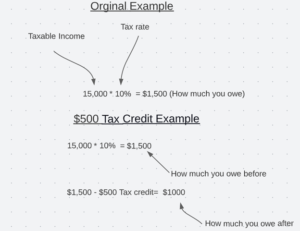

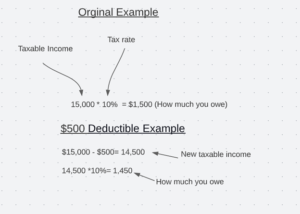

Say you have 15k of taxable income. Based on your income, you landed in a tax bracket where you have to pay 10% of 15k to the government.

If you have 15k of taxable income and pay 10% of that income in taxes, you will owe $1,500 in taxes.

However, what if you were to get a $500 deductible? Well, that deductible would be taken from your taxable income.

It would look something like this…

This example shows that a $500 tax deduction reduced the taxable income to $14,500.

That $14,500 is the new taxable income that will be taxed at the 10% rate—bringing us to a new total of $1,450 owed in taxes!

This is how tax deductions work. It reduces the amount of money the government can tax.

What Are Tax Credits?

Tax credits work a little differently from tax deductions. Tax credits subtract the total amount from what you owe to the IRS.

Our government offers various tax credits, and each has its own eligibility requirements.

Generally, tax credits are awarded to people who do things that benefit society.

Doing things like adopting a child, saving for retirement, and continuing education will enable you to apply for tax credits.

Even so, in essence, they all function the same way. They all reduce how much you owe in taxes.

Here is another illustration of how it works:

As you can see in this example, calculating how much you owe with tax credits is simpler because it subtracts how much you owe dollar for dollar.

Types Of Tax Credits

There are two types of tax credits available: refundable and non-refundable.

For refundable tax credits, if how much you owe in taxes is less than how much tax credit you receive, then the IRS will send you the remaining payment as part of your tax refund.

Some tax credits that exceed how much you owe can also be rolled over to the next tax year. You can still receive refundable tax credits even if you don’t own any taxes for the year.

The standard kind of tax credit that most people will receive is non-refundable. That means any portion that exceeds how much you owe in taxes will not be refunded back. You’ll just owe $0 in taxes.

Which is better?

Now, if you have a choice between one of the two options, which one would be more beneficial? Well, tax credits would be the better choice.

Tax credits are more favorable than tax deductions because tax credits reduce your tax liability dollar-for-dollar. While a deduction still reduces your tax liability, it only does so within your marginal tax rate.

When comparing the math in our two examples above, you can see that having a $500 tax credit saved $450 more than having a $500 deductible.

To Summarize

Tax deductions reduce your taxable income. On the other hand, tax credits will reduce how much you owe to the government. They are two legal methods of writing off taxes and staying on good terms with the IRS. However, tax credits save you the most money out of the two options.

{kind=link}

{kind=link}

{kind=link}

{kind=link}